Policies may cover neighborhood care, which usually means adult daycare, and break care to provide you, the caretaker, a break. Some policies may even pay advantages to family members who serve as caretakers or cover home adjustments, such as adding wheelchair ramps or setting up safety gadgets. Most policies cover care related to Alzheimer's or other kinds of dementia, however there are exceptions. Since this is a common condition, double check that it's consisted of in your enjoyed one's policy. Besides what's covered, you ought to also understand surprise coverage exclusions that might prevent gain from being paid. While modern policies have less exemptions than their predecessors, they still exist, so look out for them.

Many individuals need long-lasting care because of increasing frailty, persistent disease, dementia or Alzheimer's, which don't constantly demand hospitalization immediately prior to they require long-lasting care. If the prerequisite isn't satisfied, it could keep your loved one from ever certifying for benefits. A lot of states have actually outlawed business from including this exclusion, but it's still legal in some. A lot of long-lasting care insurance coverage completely leave out advantages being paid for specific conditions. Look out for common conditions excluded, such as particular types of cardiovascular disease, cancer or diabetes. Other exclusions consist of: Psychological or worried conditions, not counting Alzheimer's or other dementia, Alcohol or substance abuse, Tried suicide or deliberate self-harm, Treatment in a government center or currently paid for by the government, Illness or injury caused by an act of war Policies released to insurance policy holders with pre-existing conditions generally include a temporary exclusion. Pre-existing conditions normally will not be covered for a set time period.

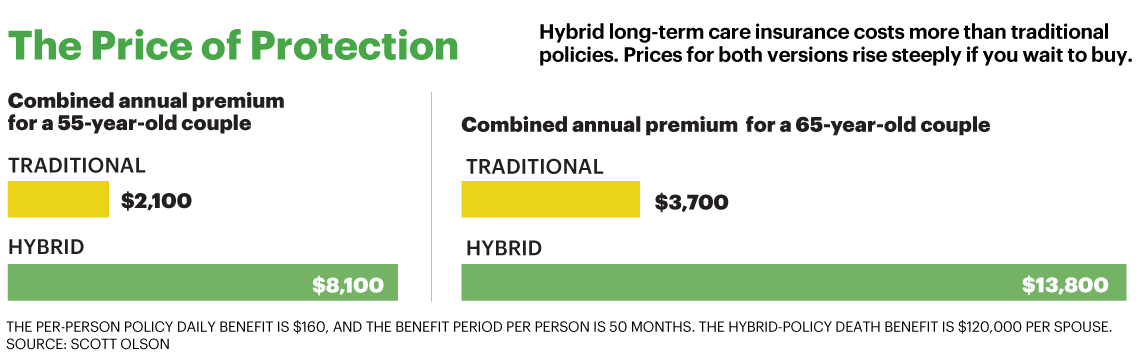

Avoid policies with exclusion durations longer than 6 months. There aren't any age limitations on when you can acquire long-term care insurance, however it's more expensive and harder to get approved the older you get. For this factor, the majority of people purchase their policies in their 50s or early 60s. Insurer may recommend acquiring a policy as young as 40, however Customer Reports advises waiting till age 60 - How to get health insurance. Once an individual hits their 70s, a great long-term care policy becomes extremely pricey, and it may be incredibly hard to certify for coverage, especially if they currently have health problems. According to the AALTCI, couple of insurance provider even use protection to anybody over the age of 80 and a person over 80 who in fact passes the health qualifications most likely would not be able to pay for the premium.

If they wish to https://holdenvzaf075.wordpress.com/2021/08/07/getting-my-who-owns-progressive-insurance-to-work/ be genuinely covered versus the high costs of long-term care at all times, they must buy long-term care insurance as quickly as they have possessions that need defense and can afford the premiums. It's never ever prematurely to consider buying long-lasting care insurance coverage, advises Duane Lipham, a Licensed Long-Term Care expert. As you're helping your enjoyed one purchase their policy, you may likewise wish to think about coverage for yourself if you fulfill the requirements since special needs isn't restricted to age limits. If your liked one is primarily concerned about safeguarding their possessions in retirement, at what age does it make the most affordable sense for them to seriously consider purchasing long-lasting care insurance coverage? Lipham usually advises buying at a more youthful age, somewhere between the ages of 45 and 55, for 2 primary factors: It's fairly budget friendly.

The majority of people typically still enjoy a procedure of excellent health at this phase in life and can get extra premium discounts for having a good health history. They can lock in these lower premium timeshare costs rates for the remainder of their lives. After the age of 55, Lipham warns that premium costs do begin to accelerate more rapidly and increase significantly from year to year in an individual's mid-60s. The course of financial wisdom is to buy long-lasting care insurance coverage earlier rather than later, when premiums are low. While searching for long-lasting care insurance coverage for someone in your care, talk to their present or former employer, life insurance supplier or insurance broker to see if they can add protection to an existing policy.

Contact independent agents who offer policies from numerous business rather than a single insurance company to get a number of options from a single source. Picking the best strategy from all these options depends upon several elements. Age impacts the expense of the picked strategy, and picking the ideal features, especially the day-to-day advantage and inflation defense, impacts the care received. Compare plans carefully to guarantee your loved one finds a budget friendly policy that doesn't sacrifice protection. Speak with an older law lawyer or financial planner if you have any questions. If you have actually already purchased insurance however discover it's not what you thought, a lot of states need a 30-day cancellation duration.

5 Simple Techniques For How Much Is Car Insurance Per Month

Like any insurance, long-term care insurance is a monetary gamble (What is renters insurance). Your loved one is wagering years of premiums versus the probability of a long stretch of expensive long-term care. Ought to they decide to take the gamble, make certain they get a policy with premiums they'll be able to manage for numerous years because their regular monthly income may change and the premiums will increase. As an included precaution, search for policies Check out this site that provide some refund defense if after a rate trek the policyholder can't keep paying the greater policy premiums. A good refund provision can make one policy more appealing over other comparable alternatives.

The daily benefit is how much the policy pays out in advantages for each day the insurance policy holder requires care. Some policies pay advantages based on an everyday limitation, and others multiply that day-to-day amount by 30 to establish a regular monthly advantage quantity. You can easily help your enjoyed one determine an affordable everyday benefit amount by calling local nursing centers and home healthcare agencies to discover the average cost for these services in your area. When calling regional centers, make sure to ask what the expenses are for long-term care rates and not short-term rehabilitation. Also, ask for rates for both personal and semi-private rooms because there's frequently a substantial cost difference.

When you have an excellent idea of the everyday costs involved in local long-term care, decide just how much of that everyday quantity you feel your liked one could reasonably co-insure out of their own funds. When making this estimation, remember that whatever funds they'll offer for their own care needs to be kept in a readily accessible financial investment vehicle so they can access these funds quickly if and when they require to. Some people think they need to over-inflate the day-to-day benefit total up to ensure they equal the increasing expenses of care. It's true that long-lasting care costs are rising so quickly that an ideal daily advantage today may be just half of what is needed in simply 15 years or so.